Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Relief is coming for UK mortgage holders. But not, like, very much of it.

A Barclays note published today lays out a looming “positive impulse to consumption” as flexible mortgage holders (a minority of a minority) and people on shorter fixed-term mortgage (a minority of a majority of a minority) start to feel that sweet, sweet interest-rate relief:

We wrote about mortgages a bit last summer, looking at how the shifting composition of UK home borrowing to (mainly 5-year) fixed terms had shifted monetary policy transmission dynamics from “a rising rate tide gently splashes all ships” to “f*** you specifically to the ships built in 2017-18”.

Some things haven’t changed. To shamelessly reuse a meme:

(We’d love to talk about renting more. The problem from the perspective of a markets and finance blog is that mortgage-market dynamics hinge on quantifiable and measurable metrics, whereas the UK rental market is more like a prisoner’s dilemma in which one prisoner is banned from speaking.)

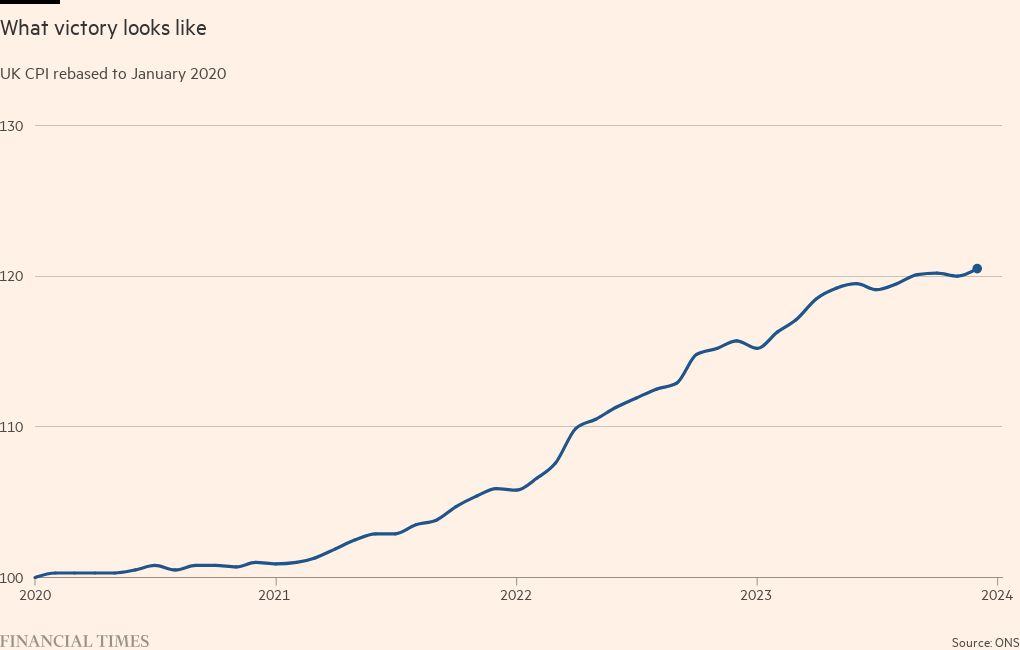

How have other things developed since then? They’ve both changed a lot and also not very much. Thanks to Rishi Sunak’s diligent efforts, the UK beat inflation . . .

. . . and Andrew Bailey is now a national hero:

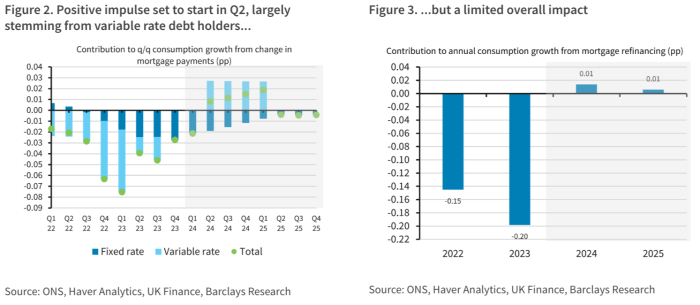

Still, growth remains an issue. Is the looming rate relief the silver bullet needed? Not really, says Barclays’ Abbas Khan.

The problem, Khan suggests, is basically the dominance of the five-year fix. Coupled with the short window when rates recently peaked, it means rate relief — like rate pain — will filter through slowly. And, in the meantime, relief just means less pain:

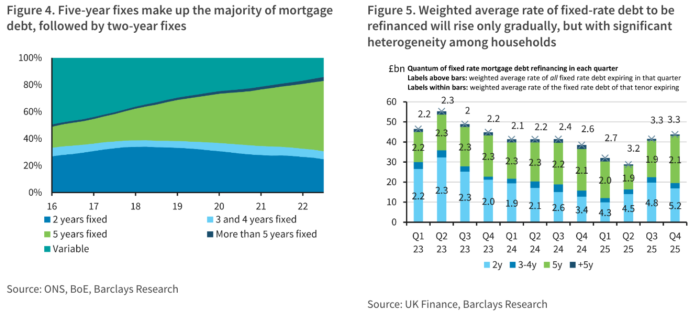

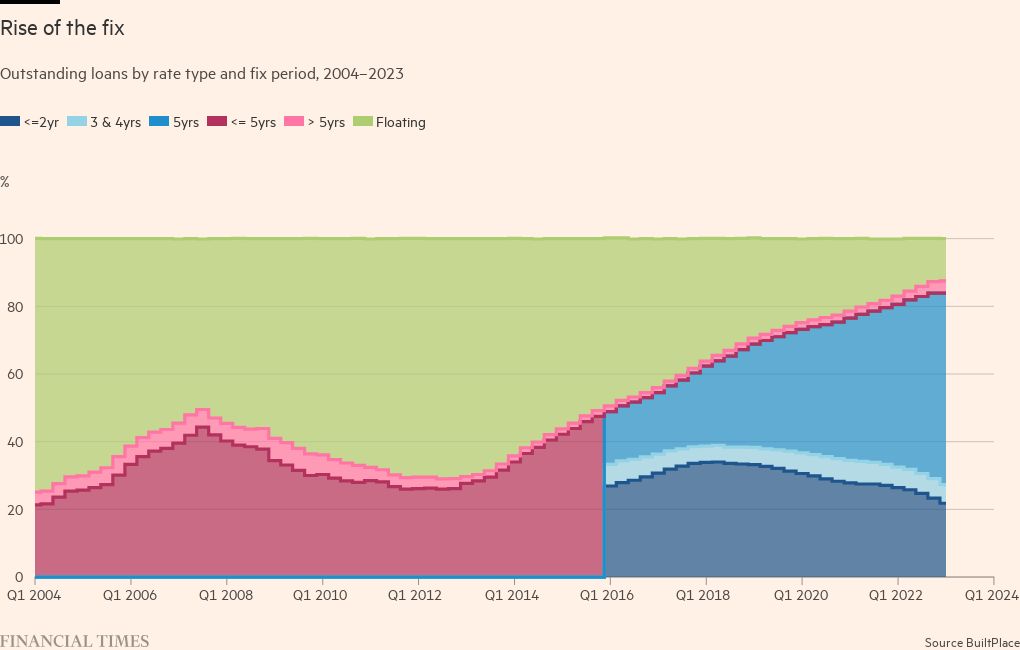

A large majority (85%) of mortgage debt is fixed-rate, typically for two or five years. This was not always the case: the proportion of variable rate debt has fallen sharply over the last decade, from a peak of c.70% in 2012. Rate changes take longer to feed through to fixed-rate debt holders, which will limit the overall boost to consumption during the cutting cycle.

Even on our baseline 200bp cutting cycle, households on five-year fixed rate mortgages (around half of total mortgage debt) that refinance over the next two years are likely to face increased mortgage payments as they had locked in rates prior to the recent hiking cycle (though this would not be the case if rates were to rapidly fall to below levels seen at the onset of the pandemic…

Meanwhile, households on two-year fixed rate mortgages are also likely to be refinancing on higher rates through 2024 even while Bank Rate is being cut. However, those refinancing through 2025 should eventually be able to refinance at lower rates (ie, with reduced mortgage payments) since their existing rates were locked in well into the hiking cycle. Hence, through 2025, mortgage refinancing will likely become a boost to this cohort’s income…

Accordingly, even on our baseline for rates and taking into account the swift pass-through of cuts to variable rate debt, the overall impulse from mortgage refinancing on aggregate consumption is likely to be close to zero for both 2024 and 2025.

We’ve reversed the order of these two chart pairings to maintain the punchline:

Barclays’ credit team suggests this rather meagre boost could benefit “grocers, pubs and gyms”, so, you know, whatever.

More interesting is Khan’s analysis of the counterfactual: a world in which the UK never developed an affection for fixed rates. As a reminder, let’s recycle a (slightly dusty) chart from Toby’s piece last June on how the long-term composition of mortgages has shifted:

Comparing the actual share of variable-rate mortgages with the recent-ish high in 2012 (when about 70 per cent of mortgages were floating), Khan models a bigger rebound after a far, far worse dip:

What can we learn from this? One perspective is that the UK just got lucky: 2012–2013’s mortgage market wouldn’t have weathered the post-pandemic rate cycle anywhere near as smoothly as 2022–23’s mortgage market did.

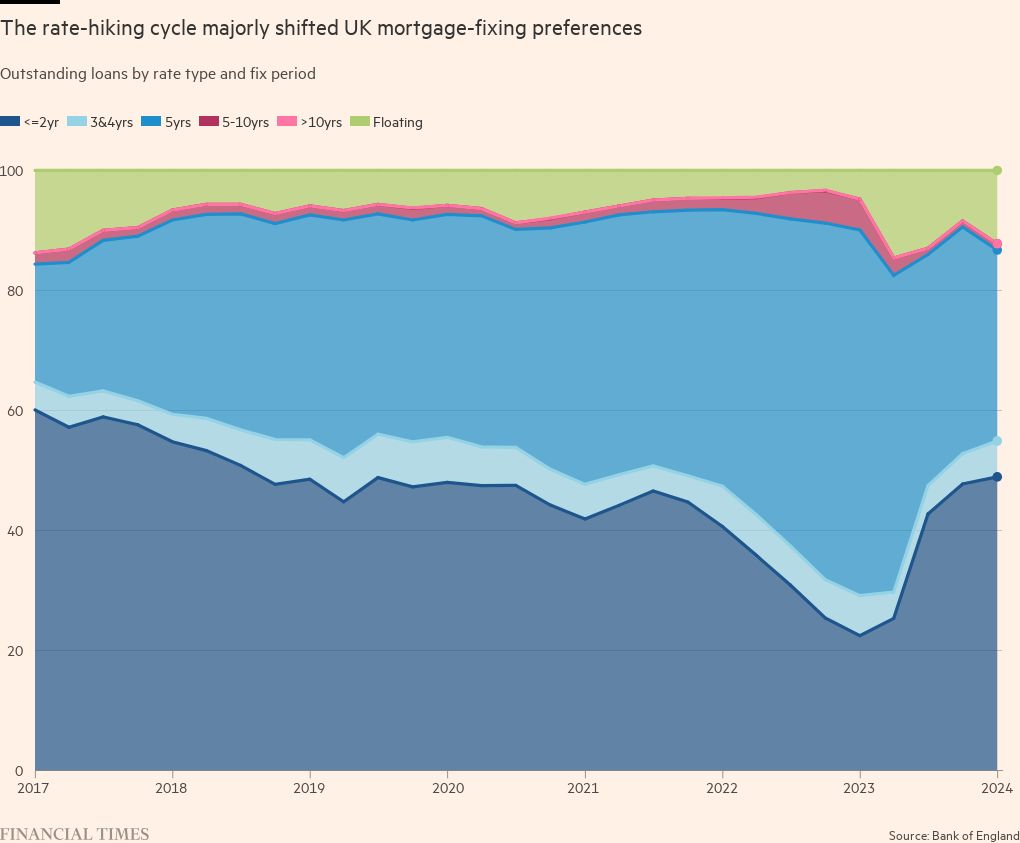

A potential blind spot in Khan’s analysis, however, is an apparent reliance on slightly out-of-date mortgage data. Barclays’ chart (figure 4 above) runs to the end of 2023. But the latest data from the Bank of England suggests that was roughly the point at which behaviour changed, and a lot more mortgage borrowers tilted towards shorter-term fixed rates:

Look at that squeeze on the 5-year! Assuming Barclays used the slightly older data, this suggests the midterm boost to incomes could be more front-loaded than the bank predicts.

In the longer term, it will be interesting to see whether this cohort — the unhappy victims of monetary policy transmission through the modern mortgage market — changes its behaviour.

If so, the manner of change might be hard to predict. Let’s imagine a woman called Sarah (which Google suggests is one of the most popular names of the 1980s) in her mid-thirties:

— In early 2018, Sarah buys a house with a five-year fixed-rate mortgage at a very, very low rate.

— In early 2023, Sarah has to renew her mortgage, and finds rates have massively increased. She reads the Financial Times, and learns that rates will probably come down in the not-too-distant future. Instead of getting a new five-year fix, she gets a two-year fix.

— In early 2025, she once again renews her mortgage. She is offered a lower rate than her 2023 mortgage, but still much higher than her original one in 2018.

What happens then? Does the bitter memory of 2023 prompt Sarah to get a longer-term fixed mortgage (eg a 10-year) for a greater period of stability at lower rates? Does she bet rates will fall further and get another 2-year? Does she accept a new normal of higher rates and return to the 5-year default?

We certainly hope you’re not expecting us to have the answer, but it will be interesting to see what the Sarahs of the UK do.

{kind=link}