Big investors are selling US Treasuries and buying European government bonds, betting that cooler inflation in Europe will allow its central bank to start cutting interest rates sooner than the Federal Reserve.

Money managers at Pimco, JPMorgan Asset Management and T Rowe Price have all increased their exposure to European government debt in recent weeks.

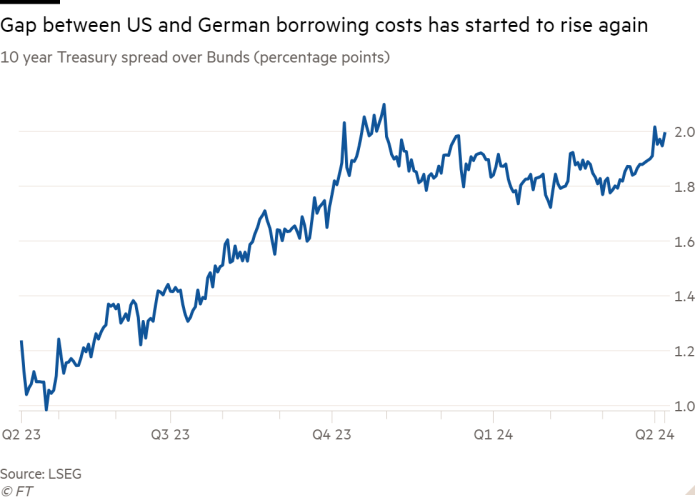

That has helped push the so-called spread, or gap, between benchmark 10-year German and US borrowing costs to 2 percentage points, close to the highest level since November.

“The path for rate cuts in Europe is clearer than in the US,” said Bob Michele, chief investment officer and global head of fixed income at JPMorgan Asset Management. “It is hard to find an economic reason for the Fed to cut rates.”

He added that he currently has a larger than usual holding of European government bonds and has been “moving in [the] direction” of acquiring more.

The shift comes as the US and European economies have begun to diverge, with softer inflation and a weaker economy in Europe fuelling bets that the ECB will deliver more cuts than the Fed this year.

Markets are currently pricing in three or four ECB rate cuts by the end of the year, compared with only two or three for the Fed.

Government bonds on both sides of the Atlantic have sold off this year, pushing yields higher, as investors scaled back their expectations of imminent rate cuts.

However, the moves have been greater in the US, where the benchmark Treasury yield has risen by 0.5 percentage points to 4.4 per cent. In comparison, the equivalent German Bund is up 0.3 percentage points to 2.4 per cent.

Andrew Balls, chief investment officer for global fixed income at Pimco, said he had favoured European government bonds and UK gilts over US Treasuries this year because there is “more evidence of inflation correcting” there.

Pimco, which manages $1.9tn in assets, lowered its forecast from three to two quarter-point rate cuts by the Fed this year, following a blockbuster jobs report on Friday.

Economists expect US inflation data for March, released on Wednesday, to show an annual rise to 3.4 per cent. Readings for January and February have already come in above analysts’ forecasts.

By contrast, Eurozone inflation fell to 2.4 per cent last month, lower than forecast, bolstering expectations that the ECB will cut interest rates by the summer.

“We prefer to be underweight in US Treasuries in favour of Eurozone bonds including Bunds,” said Quentin Fitzsimmons, a senior portfolio manager at T Rowe Price, which manages $1.4tn of assets globally.

He said his conviction about an ECB rate cut in June was “high”, while strong US data had caused the Fed to “backpedal from its hitherto clear desire to start to cut interest rates”.

Fitzsimmons said that if the ECB did start cutting faster than the Fed, the lower rates would reduce the hedging costs of holding bonds in the eurozone compared with US Treasuries.

He said this would “possibly encourage more capital to back the idea of relative outperformance by Bunds in relation to US Treasuries”.

But some analysts warn that if the ECB gets too far ahead of the Fed in making rate cuts, the euro could weaken significantly, risking another upturn in inflation.

“There can only be so much divergence before it starts to have a big currency impact,” said Mike Pond, head of global inflation-linked research at Barclays. “It might be difficult for the ECB to cut as much as we’re expecting if the Fed doesn’t cut as well.”

Nevertheless, the inflation outlook is currently more benign in Europe than in the US. The European Central Bank estimates annual inflation in the eurozone will be 2.3 per cent in 2024, with growth of 0.6 per cent.

That compares with the Fed’s projection that the core personal consumption expenditures index — the US central bank’s preferred inflation gauge — will cool this year to 2.6 per cent, from the current rate of 2.8 per cent.

The US central bank estimates that growth will be 2.1 per cent by the end of the year.

“Growth in the US has been shown to be more resilient than in Europe,” said David Rogal, a portfolio manager at BlackRock. He added that this was partly due to the US having a relatively closed economy and heavy government spending.

Europe, he said, has “a more open economy with more sensitivity to global manufacturing developments, as well as less of the fiscal impulse”.

Rating agency Fitch forecasts that the US government’s budget deficit, the difference between its total expenditures and revenues, will be 8.1 per cent of gross domestic product this year, compared with 1.4 per cent for Germany.

{kind=link}