Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Cracks in US commercial property markets are spreading. Over-leveraged and underused office buildings in New York and San Francisco are starting to trade hands at knockdown prices. Banks are being forced to mark down loans to realistic levels. Provisions and losses are growing. US regional banks are most exposed but lenders in Europe, particularly specialist German real estate banks, are also on the hook.

Credit agencies recently downgraded the German lenders Deutsche Pfandbriefbank and Aareal Bank. US exposure accounts for about 15 per cent of their real estate lending books. However, they are also among the largest commercial real estate lenders in Germany, where Deutsche Bank leads, followed by state-owned Landesbanks LBBW and BayernLB. Commercial property markets in Germany are so far faring better than the US but America’s pain is likely to spread.

The best analogy for the office market today is the turmoil of retail property following the online shopping boom last decade, thinks Nicola De Caro at ratings group DBRS Morningstar. The enduring popularity of working from home has slashed demand for space, with vacancy rates in some US markets now pushing 20 per cent.

European demand, particularly on the continent, is holding up better with more office-based working. But markets have divided into “the best and the rest”, with new ESG-compliant buildings in demand and older stock firmly out of favour.

When it comes to office valuations, there is surprisingly little difference between US and European markets, says Peter Papadakos of Green Street. Both have experienced falls of as much as half. But higher US rates exacerbate problems — debt costs have risen from 3 per cent in 2021 to about 8 per cent today. Compare that with increases in Europe from 1.5 per cent to between 5-6 per cent. Better hedging and a more borrower-friendly approach by European lenders have supported the financing environment.

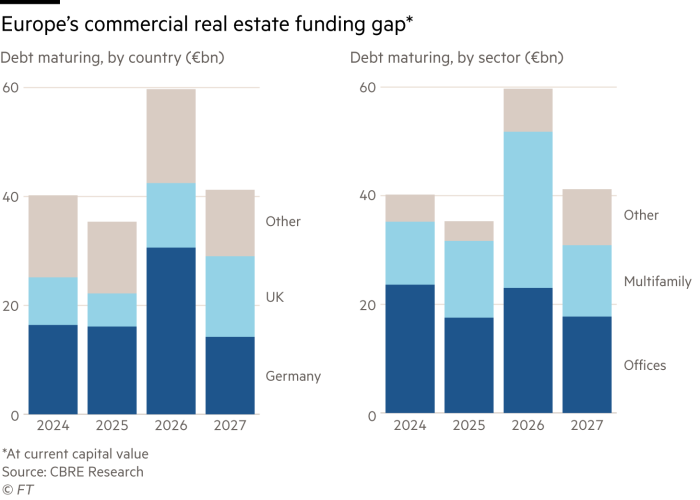

The question is for how long? A looming financing gap suggests time is ticking. Some €40bn of European commercial real estate debt is expected to mature this year, according to CBRE. About two-thirds of that figure are loans to offices and about half of the total relates to properties in Germany.

Maintaining the status quo appears dependent on the European Central Bank cutting interest rates. “Conditions have certainly blown loan-to-value ratios out of covenant levels for many developers and owners,” said Saul Goldstein, founder of distressed fund ActivumSG.

Banks are already feeling the squeeze as bad US loans are marked to market. Rising losses and a wave of distressed asset sales look inevitable in Europe too.

Lex is the FT’s concise daily investment column. Expert writers in four global financial centres provide informed, timely opinions on capital trends and big businesses. Click to explore

{kind=link}