The annual state pension could surpass £13,000 a year by 2030 if the current pension triple lock is retained, analysis claims.

Both the Conservative and Labour parties are expected to pledge their support for the pensions triple lock in their manifestos for the upcoming general election, according to media reports.

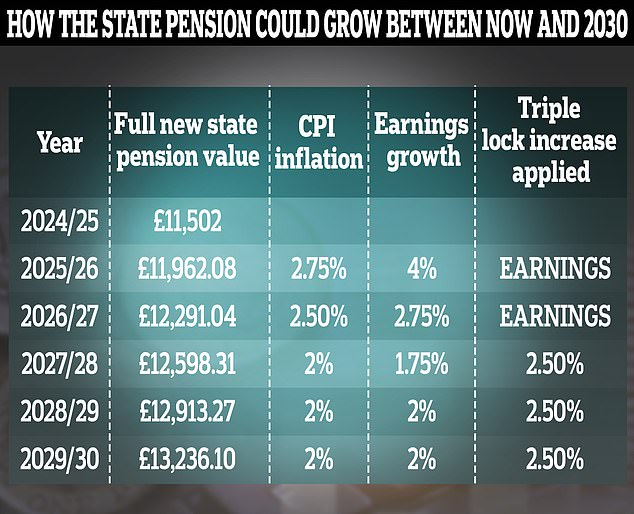

Under the triple lock, state pensions could reach £13,236.10 in 2029/30, after surpassing £12,000 in 2026/2027, according to research by investment platform AJ Bell.

The state pension is set to surpass £13,000 by 2030, and many more pensioners will end up paying income tax if the £12,570 personal allowance is not raised before then

However, analysis from the Mail on Sunday warns that more pensioners could be dragged into the lowest income tax bracket from 2027, even if the state pension is their only income.

The warning comes after Chancellor Jeremy Hunt confirmed that the Government will maintain the £12,570 tax-free personal allowance until 2028.

The triple lock, brought in by the coalition government in 2011, ensures that the value of the state pension is not outstripped by the cost of living or the growth in earnings of the working population.

This means that the state pension will be increased by the highest of average earnings growth, inflation or by 2.5 per cent per year.

AJ Bell’s analysis was based on estimates of which will be used to set the state pension in coming years.

Tom Selby, public policy director at the firm, said: ‘Retirees will no doubt be rejoicing that both major parties appear set to recommit to the state pension “triple-lock” for the next Parliament, with the gold-plated pledge potentially pushing the value of the state pension past £13,000 a year by the end of this decade.

‘Given how critical the votes of older people are to winning a general election, it is no surprise both the Conservatives and Labour appear to be taking a safety-first approach to the triple-lock,’ Selby said.

‘The policy has become a totem for “doing right by pensioners”, with debate over the state pension often restricted solely to politicians’ commitment to increasing the benefit by the highest of average earnings growth, inflation or 2.5 per cent.’

Both Labour and the Conservatives plan to retain the pension triple lock in their upcoming election manifestos, according to media reports

From April, the full state pension is set to rise by 8.5 per cent to £11,502 per year, or £221.20 a week, under the new flat rate, while those who retired before 2016 will see their pension rise to £169.50 per week.

People on the basic rate, however, also get top-ups, called S2P or Serps, if those were earned earlier in life.

Currently, the full state payout sits at £10,600, or £203.85 for those who retired after 2016, while those who reached state pension age before April 2016, get £156.20 a week.

According to AJ Bell, the move to retain the triple lock is one of relative political safety in the short-term, but could lead to ‘intergenerational unfairness’ if planned pension age hikes are accelerated.

Selby said: ‘While the policy is understandably popular, it remains entirely aimless, with neither major party clearly stating how much they believe the state pension should be worth.’

‘The next government needs to set a clear plan for the state pension, both in terms of what a “fair” value is, perhaps as a proportion of average earnings, and the length of time retirees should be in receipt of it on average.’

‘For this necessary reform to happen, politicians will need to show bravery and step beyond the current “Will they? Won’t they?” debate over the triple-lock,’ Selby added.

‘The state pension remains the bedrock upon which people’s retirement plans are built, so embedding at least some certainty into the system is crucial to help Brits plan with confidence.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

{kind=link}