Introduction

In the ultra-competitive and fast-moving world of sports data, odds and video streaming, there are four key players in the space, namely Sportradar (NASDAQ: $SRAD), Endeavor Group Holdings, Inc (NYSE: $EDR), Genius Sports Group (NYSE: $GENI) and Stats Perform (unlisted).

I will only be dealing with $SRAD, $EDR and $GENI as their financial performance is publicly accessible, while Stats Perform is not.

I will seek to provide the investment thesis, risks, valuation and a conclusion for each of the three listed companies.

However, I firmly believe that the majority of sports data and betting stocks – particularly those online – would be a positive addition to any diversified portfolio.

Summary

$SRAD have the business model as well as the momentum (due to the ATP rights acquisition and sustained profitability) to win the arms data race.

$EDR, long term, will survive and have the tools to recover from their crippling debt although its sports betting arm, IMG ARENA is, as yet, unproven.

Finally, however, $GENI can only be described as on the brink of a catastrophic collapse.

Invest in sports betting data for the long haul, but study the individual players, particularly regarding profitability, and be sure to look into each of them separately.

Background

The global sports betting market is estimated to have accounted for $83.65billion in revenue in 2022. One estimate for the World Cup in 2022 alone generated no less than $3billion in revenue. Bookmakers rely heavily on sports data and video streams to provide accurate odds and enable customers to place bets on sporting events. Reliable sports data and stable video streams are essential for several reasons:

Accurate odds: Bookmakers need reliable sports data to calculate odds accurately. The odds are based on the probability of a certain outcome occurring in a sporting event. The more accurate the data, the more accurate the odds will be, which is essential for bookmakers to make a profit and remain competitive.

In-play betting: In-play betting, where customers can place bets during a sporting event, has grown exponentially in recent years. To offer in-play betting, bookmakers need real-time sports data and video streams to enable customers to place bets quickly and accurately.

Fraud prevention: Reliable sports data and video streams are also essential in the fight against fraud. Bookmakers use sophisticated algorithms to detect and prevent fraudulent activity, such as match-fixing or insider trading. Reliable data and video streams help bookmakers detect anomalies in the betting patterns and prevent such activity.

Customer experience: Stable video streams are essential for customers to enjoy a seamless betting experience. If the video stream is buffering or unstable, customers may become frustrated and lose trust in the bookmaker’s platform. This can result in a loss of customers and revenue for the bookmaker.

Without these four essential components, bookmakers would struggle to compete in the highly-competitive sports betting industry. Therefore, our target companies $SRAD, $EDR and $GENI play a key part in generating this revenue for bookmakers and take their own share as any key supplier should.

Business Model

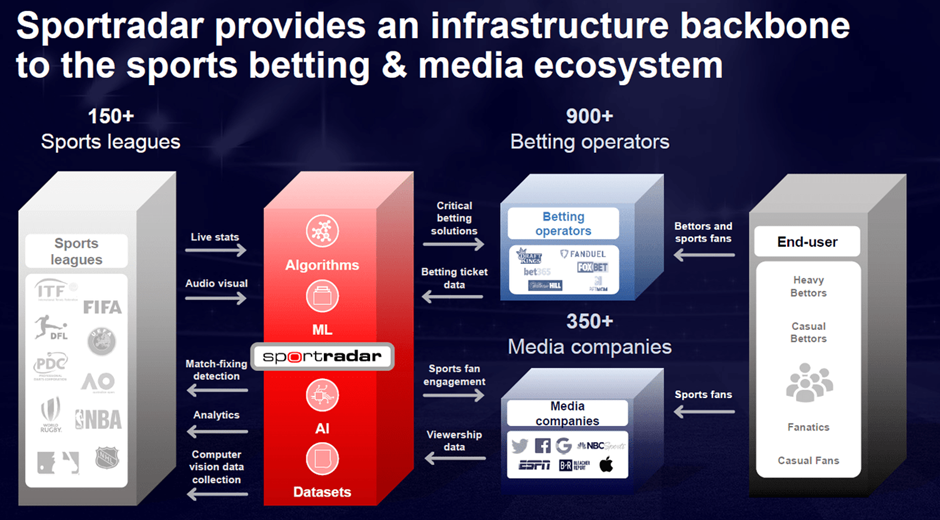

While there are variations, all three companies adhere to a similar business strategy which is best described by the below graphic:

SRAD – 3Q21 Earnings Presentation – vF

In essence, sports data companies buy statistics and video content rights (and offer products in return to lessen the cost burden) from sports leagues. By developing algorithms and applying machine learning, they are able to add value and sell newly-created products to sports betting operators and media companies who in turn provide fans with content to keep their eyes glued to their websites and video platforms.

IMG ARENA, the sports betting arm of $EDR describe their business model as follows:

“… IMG ARENA, provides data and content to sportsbooks and media partners around the globe, delivering data feeds from approximately 43,000 sports events annually. This data powers IMG ARENA’s Event Centre product suite, including the UFC Event Centre. In addition, IMG ARENA provides live video streams for sportsbooks for approximately 48,000 events per year, as well as a portfolio of virtual sports products. We leverage the technology derived from IMG ARENA to provide streaming video solutions to our clients and our owned assets via Endeavor Streaming. In addition, we closed our acquisition of leading B2B sports betting technology provider, OpenBet…”

$SRAD

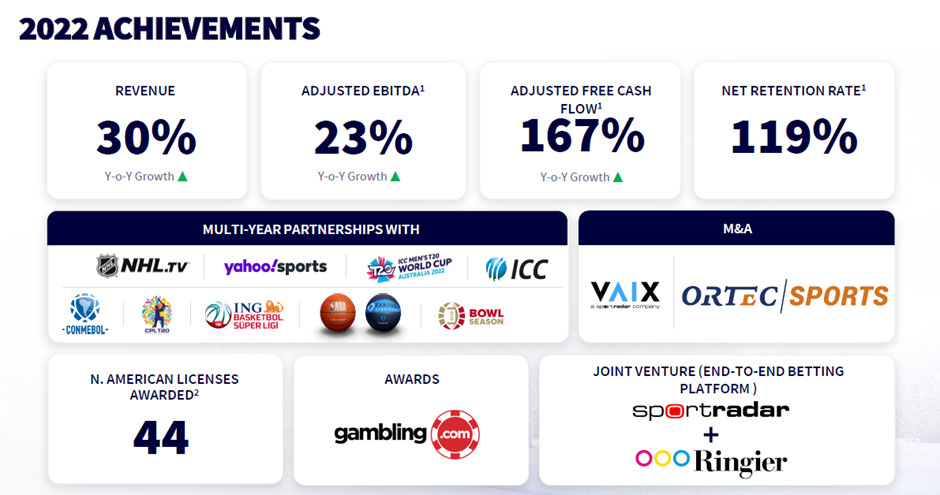

While Q1 results will be announced on May 10 2023, Q4 and 2022 FY results were excellent and helped stabilise the company’s stock price during the months of March and April.

2022 Results

SRAD Q4 2022 Earning Presentation March-FINAL (1)

30% revenue growth for a company founded in 2001 shows a company continuing to innovate and their 167% YoY growth (€39million) in Adjusted Free Cash Flow was music to investors’ ears rebuffing the accusation that sports betting companies can’t make profits. Multiyear partnerships with International Cricket Council (ICC) and the NBA-FanDuel deals were particularly standout. And to add to the good news was the acquisition of Vaix and Ortec Sports. Vaix, in particular, is described in the 2022 annual report:

“On April 6, 2022, the Group acquired 100% of the voting interest in Vaix Limited (“Vaix”), a private company incorporated in England and Wales with a wholly-owned subsidiary incorporated in Greece, Vaix Greece IKE. Vaix develops artificial intelligence (AI) solutions for the iGaming Industry. Vaix’s innovative AI technology allows betting and gaming operators to gain a personalized view of their customers, which provides a more targeted, player-friendly experience. The Group paid at closing a purchase price in cash of €21.7million.”

If $SRAD – a notably cautious business – is paying close to $25million for an artificial intelligence company, this is a clear indication of the way market trends are shifting.

Risks

In their annual report, $SRAD lists over 20 risk factors and these range from generic to the highly specific, but one in particular stands out:

“failure to, maintain, protect, enforce and defend our intellectual property rights, or to obtain intellectual property protection that is sufficiently broad, may diminish our competitive advantages or interfere with our ability to develop, market and promote our products and services;”

This suggests $SRAD has some IPs of significance to protect and is concerned with monetizing those products and services which were expensive to deliver to market. As far as long-term investors are concerned, time will tell, and it will be seen in the annual growth rate. With 2023 guidance pegged at $1.1billion which is another healthy 25% increase, meeting such a number would validate the investment in the aforementioned technology.

Valuation

As of May 1 2023, $SRAD sits at $11.57, market cap of $3.44billion, a 12- month range of $7.10 to $14.59, a 2022 revenue multiple of 4.8X and a P/E ratio of 270+ which sits below the average for the Information Services industry of 1600x and often negative for trailing 12 months figures. For instance, Palantir Technologies (NYSE: $PLTR) currently boasts -43.1.

Google Finance: SRAD, May 1st 2023

The graph shows a sharp decline which followed the global tech stocks trend and a stable recovery from July 2022 with $SRAD buoyed by consecutive quarters of growth and successfully hitting EPS analyst targets. As previous articles have pointed out, $SRAD can be bought at a discount with no apparent change to the business model or industry landscape. I do not think it unreasonable for $SRAD to reach $14.00 by year end, which is also the price target JP Morgan posted last month.

$EDR

$EDR’s situation cannot be viewed in isolation due to the fact that IMG ARENA sits within Endeavor Holdings Limited, Inc. To try to gain an insight into $EDR’s performance, I looked at the overall group’s latest quarterly earnings. Similar to $SRAD, 2023 Q1 results will be released on May 9 2023.

2022 Results

There are few clues within $EDR’s filings and earnings transcript as to IMG Arena’s input. But we can see the following:

● “Beginning January 1, 2023, we created a fourth segment, Sports Data & Technology, which includes our IMG ARENA and OpenBet businesses.”

● “In September 2022, we acquired the OpenBet business (“OpenBet”) of Light & Wonder, Inc. (formerly known as Scientific Games Corporation) (“Light & Wonder”) for consideration of $847.1 million”

● “With this business built out, we’ve created a fourth segment sports data and technology. On the balance sheet, we continue to execute with financial prudence. We promised last year we would get our net leverage below 4x by year end. We delivered on that promise closing out 22, having paid down $0.5 billion of debt, and we will continue to pay down debt in 2023. Looking ahead, we believe in the strength of our portfolio and the durability of our long-term strategy.”

Overall, I can only deduce that IMG ARENA is not profitable at present. In any event, $EDR as a business is not profitable, showing a net income loss of some $322million in 2022.

Risks

In their Form 10-K (2022 Annual Report), $EDR refer to two key risks. One is an isolated reference which uses the phrase “our substantial indebtedness” which is later clarified as “As of December 31, 2022, we had an aggregate of $5.1 billion outstanding indebtedness under our Senior Credit Facilities…” This will cause several issues in the future:

- The need to dedicate a significant portion of their cash flow to pay off their debt

- The need to refinance imminently

- Potential downgrade of credit rating

- Which leads to increased cost of borrowing

- Inability to obtain working capital

But it is the second risk which forewarned a major change in the rights acquisition landscape. Under Competition, “The entertainment, sports, and content industries in which we participate are highly competitive. We face competition from alternative providers of the services, content, and events we and our clients and owned assets offer and from other forms of entertainment and leisure activities.”

And then, in March 2023, Sportradar won the six-year betting data and video streaming rights for the ATP – a competition with a huge volume of content (14,500 matches). Without the rights to the ATP, it is going to be a real problem for IMG ARENA to secure a larger market share of monetizable rights, especially as all the major competitions are bought up for multiple years in advance.

Valuation

As described, $EDR’s data and streaming rights business represents only a fraction of their overall revenue which totalled $5.3billion in 2022. But with 2021’s revenue noted as $5.08 billion, 3.75% growth is hardly exciting, compared to $SRAD’s 30%.

Google Finance: $EDR, May 1st 2023

$EDR is valued differently to $SRAD or $GENI at just 2x 2023 forecast revenue. However, with the sudden loss of the ATP rights and the upside of OpenBet’s revenue cancelled out by the hefty purchase price they paid, $EDR should be swerved until further notice.

$GENI

In almost perfect symmetry, $GENI will release their results on May 9 2023 – the same day as $EDR and 24 hours after $SRAD. It will be a busy time for analysts and a nervous one for investors. In particular, these results will be crucial for investors who want to assess whether $GENI can sustain their business model in the face of dual threat of the rising cost of rights and fierce competition which has been gradually eroding their market share.

2022 Results

Zacks Equity Research summarised $GENI’s 2022 Q4 earnings, but it was not complimentary. Here is an extract from that report: “Genius Sports Limited (GENI) came out with a quarterly loss of $0.18 per share versus the Zacks Consensus Estimate of a loss of $0.11. This compares to loss of $0.44 per share a year ago… This quarterly report represents an earnings surprise of -63.64%.”

All told, $GENI lost $182million in 2022, having increased revenue 41% YoY and posting a group EBITDA of $16million. But investors spotted 2023’s revenue target of $391million which represents a YoY increase of just 15%. How can a company which grew 41% the previous year and invested hundreds of millions of dollars in technology, rights and acquisitions, only grow 15% in 2023?

Google Finance: GENI, May 2nd 2023

Risks

The greatest risk to $GENI’s existence is its inability to generate free cash flow to enable it to continue to acquire data and video rights primarily, but also technology. Only $GENI can rescue themselves by posting inflated Q1 2023 numbers.

Valuation

The big question is how does one value a company with the following losses:

| Year | Loss ($m) |

| 2022 | 182 |

| 2021 | 604 |

| 2020 | 30 |

| 2019 | 40 |

And the answer is not very highly…

Google Finance: GENI, May 2nd 2023

The current market cap of $833million is in fact only 2.13X 2023 projected revenues and could represent some positive value. However, execution risk is too high a factor in $GENI’s valuation. Investors would be perfectly entitled to take the view that sustained losses would be dangerously detrimental to $GENI’s short-term plans.

Conclusion

$SRAD, $EDR and $GENI may well have strikingly similar business models but in actuality they have very different financials.

$SRAD looks to be a promising investment for 2023 with significant percentage upside, buoyed by stable results and cash in the bank.

$EDR rely on their existing entertainment business for their valuation but are hoping to break into the betting data space with their acquisition of OpenBet.

$GENI could face serious problems if they grow at just 15% while sustaining net losses. As that wise old bird Charlie Munger, vice chairman of Berkshire Hathaway, famously said: “I don’t like when investment bankers talk about EBITDA, which I call bullshit earnings.”

{kind=link}