Halifax: Strongest annual house price growth in a year

Newsflash: UK house prices jumped in January as falling mortgage rates boosted the market.

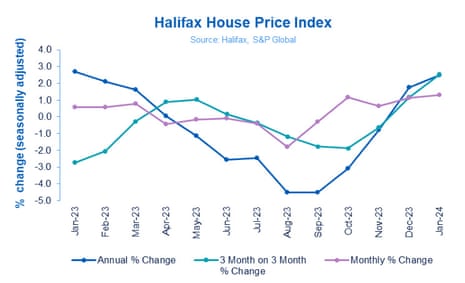

Data just released by Halifax shows that average house prices were 2.5% higher than a year ago – the highest annual growth since January 2023.

The typical UK home now costs £291,029, around £3,785 more than last month, Halifax reports.

On a monthly basis, they rose by +1.3% in January, the fourth monthly rise in a row.

However, South East England continues to see most downward pressure on house prices.

Halifax reports:

Northern Ireland recorded the strongest growth across all the nations or regions within the UK – house prices here increased by +5.3% on an annual basis. Properties in Northern Ireland now cost on average £195,760, which is £9,761 higher than the same time in January 2023.

Scotland and Wales both saw positive growth, +4% on an annual basis to £206,087 and £219,609 respectively. North West (+3.2%), Yorkshire and Humber (+2.8%), North East (+2.0%) and East Midlands (0.5%) also recorded house price increases over the last year.

The South East fell the most last month when compared to other UK regions, with homes selling for an average £379,220 (-2.3%), a drop of £8,866.

Last week, rival lender Nationwide reported that prices rose by 0.7% in January, so this is the second sign that prices picked up last month.

Key events

UK bank profitability to remain strong, says Fitch

Major UK banks will achieve a “robust” performance in 2024, ratings agengy Fitch has predicted this morning.

In a new research note, Fitch predict that the banks’ strong earnings power, capital, and liquidity buffers will help them handle the aisks arising from “the tough macroeconomic environment”.

Fitch explains:

The effects of higher interest rates on the UK economy will be increasingly visible in 2024.

This will affect the UK banks’ performance, but we expect that asset-quality deterioration, higher funding costs and competitive pressure on lending margins will affect the performance of the largest banks only slightly.

Profitability should remain strong, despite our expectations for net interest margins to contract, reflecting higher interest rates, structural hedge income, manageable loan impairment charges and controlled cost growth.

Recent increases in UK interest rates bolstered bank profits last year, attracting criticism from MPs who urged banks to pass on higher rates to savers as quickly as to borrowers.

BoE’s Breeden: Less worried that interest rates could rise further

Bank of England deputy governor Sarah Breeden is less conerned that UK interest rates will need to be raised higher to fight inflatio.

Breeden is giving a speech now to the UK Women in Economics Annual Networking Event.

In it, she explains that the pace of pay growth, and price rises by companies, will determine how soon UK interest rates should be cut.

And she says she has become “less concerned” that UK interest rates may need to be increased higher than their current 16-year high of 5.25%.

Breeden, who is a member of the Bank’s monetary policy committee, says:

As I have become more confident that persistence is likely to evolve as embodied within our forecast, I have become less concerned that rates might need to be tightened further.

Instead my focus, and indeed the focus of many on the MPC, has shifted to thinking about how long rates need to remain at their current level.

That fits with the City’s view that rates are now at their peak, and are likely to be cut at least three times during 2024. That expectation has pushed down mortgage costs in recent weeks, helping house prices to recover in January (as Halifax reported this morning).

Breeden is one of the six policymakers who voted to leave rates on hold last week, outvoting two who wanted a rise and one who pushed for a cut.

Breeden says she will be looking to see how pay growth and demand are influencing firms’ pricing decisions, when deciding if inflation is returning sustainably to the Bank’s 2% target.

In the speech, she points out that wage growth appears to have slowed, but remains in the 6%-7% range – three times higher than the Bank’s inflation target.

She also suggests that the resilience in the housing market be a signal that demand is stronger than the Bank expect.

Yesterday, fellow MPC member Swati Dhingra argued that the Bank was taking a risk by not cutting rates immediately (as she voted for last week).

Barratt-Redrow deal: What the analysts say

Barratt’s surprise all-share offer to buy Redrow looks “astute”, says Investec:

Investec told clients this morning:

The deal looks very sensible given the challenging planning and land backdrop, particularly assuming that sales rates and the profit outlook gradually improves from here.

The all-share nature of the deal is astute, retaining a robust balance sheet.

Richard Hunter, head of markets at interactive investor, says it’s a “seismic” deal:

The move is a seismic shift for the sector, reflecting not only the challenges which housebuilders have more recently faced in terms of the economic backdrop, but also a move to shore up the capabilities of two major players, with the new “Barratt Redrow” company having aggregate revenues of £7.45 billion.

Subject to shareholder and regulatory approvals, the aim is to complete the deal in the second half of this year, with Redrow becoming the premium brand in the enlarged portfolio.

Susannah Streeter, head of money and markets at Hargreaves Lansdown, says:

‘’The economic winds have not been kind to the housebuilders and Barratt Developments and Redrow clearly believe they’ll be stronger together, giving the new combined company much bigger clout to capitalise on the structural need for housing in the UK.

Redrow’s board of directors intend to unanimously recommend that shareholders vote in favour of the £2.52 billion deal, which would give them 32.8% of the combined group, with Barratt shareholders holding 67.2%.

Shares in Barratt have dropped by 6% in early trading, as the City digests its takeover of rival Redrow.

Redrow’s shares have jumped by 13%.

The combined company will have a market capitalisation of around £7bn.

Under the deal, Redrow investors will receive 1.44 new Barratt shares for each one Redrow share they own.

In the supermarket world, Sainsbury’s is unveiling plans to overhaul its supermarkets with a focus on creating more food space.

The UK’s second-largest grocer wants to become the first choice for food for more people, and keep attracting more bigger basket primary shoppers.

Simon Roberts, chief executive of J Sainsbury plc, says:

“We’re going to build on what’s driven our success since 2020. We’re determined to be First Choice for Food, ensuring more customers in more of our stores can enjoy more brilliant Sainsbury’s food.

That means more space for our food offer, while still delivering the general merchandise products customers want from us. That way, not only will we find more ways to delight new and existing customers, we will also continue growing volume market share.

Elsewhere in the store, Sainsbury’s says it will “tighten the focus” of its general merchandise and clothing ranges – which only half its customers currently buy.

The plan aims to cut costs by £1bn through improved technology and infrastructure, although it will incur one-off costs of £150m to roll it out.

It will improve its loyalty card scheme, Nectar, to offer “personalised, rewarding and integrated loyalty and market-leading retail media capabilities”.

Sainsbury’s strategy is noteworthy.

Some good elements.

Nectar360 (retail media guys!) is forecast to generate more profit…

Which means more branded signage & competitions!

— Steve Dresser (@dresserman) February 7, 2024

Roberts is also trying to cheer shareholders, by committing to a “progressive dividend policy” and a £200m share buyback in the next financial year.

Barratt and Redrow in £2.5bn takeover deal

There’s takeover drama in the UK house-building sector this morning!

Housebuilders Barratt Developments and Redrow have agreed to a tie-up which values Redrow at about £2.5bn, to create a combined group called Barratt Redrow.

Barratt is paying £2.524bn to buy Redrow’s shares, which is a 27.2% premium to last night’s closing price.

David Thomas, chief executive of Barratt, claims the deal will lead to more ‘high-quality’ homes being built:

“We have great respect for Redrow, its overall strategy, its leadership and employees, and its high-quality homes and communities.

This is an exciting opportunity to bring together two highly complementary companies, creating an exceptional homebuilder in terms of quality, service and sustainability, able to build more of the high-quality homes this country needs.

The Combined Group would leverage the respective strengths of both Barratt and Redrow, delivering significant benefits to our people, our supply chains, and – most importantly – our customers.”

Matthew Pratt, chief executive of Redrow, said:

“Redrow and Barratt combined creates a leading UK homebuilder. Together, we’ll be in a much better position to offer a broader range of high-quality and energy efficient homes to customers.

The tie-up is expected to eventually lead to savings of at least £90m a year, in three year’s time, the companies said.

House prices rise: snap reaction

Tom Bill, head of UK residential research at Knight Frank says:

“After suffering the effects of 14 consecutive rate rises last year, house prices are getting stronger as multiple interest rate cuts are expected in 2024.

The number of new buyers registering and offers being submitted have increased since lenders dropped their prices last month, which suggests demand and activity levels will only get stronger, leading to a modest a single-digit price increase this year.”

For the fourth consecutive month house prices inc. Rising +1.3% in Jan making the avg house price £291,029. Annually Scotland & Wales (+4%) & Northern Ireland (+5.3%) continued to outperform while the South of Eng (-2.3) & London (-0.4) lagged behind. @halifax pic.twitter.com/Gt01v8hXcr

— Emma Fildes (@emmafildes) February 7, 2024

Simon Gerrard, managing director of estage agent Martyn Gerrard, says:

“The figures today line up with what we’re really seeing on the ground in the housing market – last year, a lot of people put their property searches on hold to weather wider economic turbulence. Now, however, the economy has started to stabilise, and it’s encouraging that large lenders are responding the right way to inflation coming under control by bringing down interest rates.

“Though the Bank of England held the base interest rate at their latest meeting, it has started sending signals that it may start lowering them soon. This will likely be done with caution, and rates will only drop in small increments, but it could nonetheless be a real watershed moment for the housing market, prompting a groundswell of home buying activity.

The UK housing market has made a “positive start” to 2024, says Kim Kinnaird, director at Halifax Mortgages, after rising 1.3% in January (and 2.5% over the last year).

Kinnaird explains:

“The recent reduction of mortgage rates from lenders as competition picks up, alongside fading inflationary pressures and a still-resilient labour market has contributed to increased confidence among buyers and sellers. This has resulted in a positive start to 2024’s housing market.

However, while housing activity has increased over recent months, interest rates remain elevated compared to the historic lows seen in recent years and demand continues to exceed supply. For those looking to buy a first home, the average deposit raised is now £53,414, around 19% of the purchase price. It’s not surprising that almost two thirds (63%) of new buyers getting a foot on the ladder are now buying in joint names.

Looking ahead, affordability challenges are likely to remain and further modest falls should not be ruled out, against a backdrop of broader uncertainty in the economic environment.”

Halifax: Strongest annual house price growth in a year

Newsflash: UK house prices jumped in January as falling mortgage rates boosted the market.

Data just released by Halifax shows that average house prices were 2.5% higher than a year ago – the highest annual growth since January 2023.

The typical UK home now costs £291,029, around £3,785 more than last month, Halifax reports.

On a monthly basis, they rose by +1.3% in January, the fourth monthly rise in a row.

However, South East England continues to see most downward pressure on house prices.

Halifax reports:

Northern Ireland recorded the strongest growth across all the nations or regions within the UK – house prices here increased by +5.3% on an annual basis. Properties in Northern Ireland now cost on average £195,760, which is £9,761 higher than the same time in January 2023.

Scotland and Wales both saw positive growth, +4% on an annual basis to £206,087 and £219,609 respectively. North West (+3.2%), Yorkshire and Humber (+2.8%), North East (+2.0%) and East Midlands (0.5%) also recorded house price increases over the last year.

The South East fell the most last month when compared to other UK regions, with homes selling for an average £379,220 (-2.3%), a drop of £8,866.

Last week, rival lender Nationwide reported that prices rose by 0.7% in January, so this is the second sign that prices picked up last month.

Introduction: Bank of England accused of ‘‘leap in the dark’ over quantitative tightening

Phillip Inman

Good morning, and welcome to our rolling coverage of business, the financial markets and the world economy.

MPs have accused the Bank of England of taking a “leap in the dark” as it offloads hundreds of billions of pounds worth of government debt at discount prices.

A report by the Treasury committee released this morning said the central bank had failed to fully consider the broader economic consequences should the sale crystalise a loss of up to £130bn, with the government forced to make up the shortfall.

MPs said they feared the benefits of the quantitative easing (QE) programme, which has involved the purchase of £875bn of govenment debt since the 2008 financial crisis, would be reversed under a process known as quantitative tightening (QT), having knock-on implications for public spending.

Committee chair, Harriett Baldwin, said:

“It has become clear during the course of this inquiry that the decision to undertake a period of quantitative tightening is a leap in the dark for the UK economy.

“I recognise that the Bank of England does not have a crystal ball and is in uncharted waters, but more can be done to develop forecasting and modelling tools which can help us understand the risks and benefits of QT.”

The Bank of England embarked on its QE programme in tandem with other central banks to stimulate lending in the economy. But the scheme was only expected to last a couple of years and the bonds purchased were expected to be sold at a modest loss.

Fourteen years later, and following a dramatic increase in interest rates, government bonds have lost value and could be sold, depending on the path of interest rates, at an estimated £50bn to £130bn loss over the next decade.

“The Committee determines that decisions are being taken regarding vast amounts of taxpayers’ money without any regard to value for money,” the report said, adding:

“While acknowledging the need to keep monetary policy and inflation as their foremost monetary focus, the committee asks the Bank of England and Treasury to explore how value-for money criteria could be included in decisions about the ongoing pace of QT and to consider what lessons can be learned about how QE should be used in future.”

The Bank of England would only say in response:

“We welcome the committee’s report and will consider its findings carefully before responding. We continue to encourage active debate about our monetary policy decisions and their implementation”.

Also coming up today

Shares in social media group Snap are set to tumble when Wall Street opens, after missing Wall Street expectations.

Snap missed expectations for quarterly revenue growth yesterday, as it struggles to recover from a digital advertising slump. It reported a 5% increase in revenue, its second straight quarter of growth, but shares sank byover 30% in after hours trading.

Standard Chartered is sounding out UK political heavyweights as it searches for its new chair – one of the most senior roles in British banking.

The Financial Times reports that Sir Sajid Javid, former UK chancellor, and former top Treasury civil servant Sir Charles Roxburgh are both in the frame.

The agenda

-

7am GMT: Halifax house price index for January

-

7am GMT: German industrial production for December

-

8.40am GMT: Bank of England’s deputy governor Sarah Breedento give keynote speech at the UK women in economics annual networking event

-

Noon GMT: US weekly mortgage approvals

-

2.15pm GMT: MPs to question Prudential Regulation Authority over banks’ use of Amazon Web Services and Google

{kind=link}